VPAS versus VPAG: what’s the same and what’s different?

VPAS versus VPAG: what’s the same and what’s different?

Let's run through the newly agreed Voluntary Scheme and how it compares to the previous agreement.

The buzz term of the week is VPAG – the Voluntary Scheme for Branded Medicines Pricing, Access, and Growth.

It’s a new deal between the UK government, NHS England, and the pharmaceutical industry that will be implemented in 2024, replacing the current VPAS agreement (Voluntary Scheme for Branded Medicines Pricing and Access).

As a twin, I’m used to side-by-side comparisons. After all, they are often an easy approach to identify and understand what’s similar and what’s different between two things.

And so, I bring you VPAS versus VPAG.

Timeline

Both schemes are 5 years agreements with VPAS applying from 1st January 2019 to 31st December 2023, then VPAG applying from 1st January 2024 – 31st December 2028.

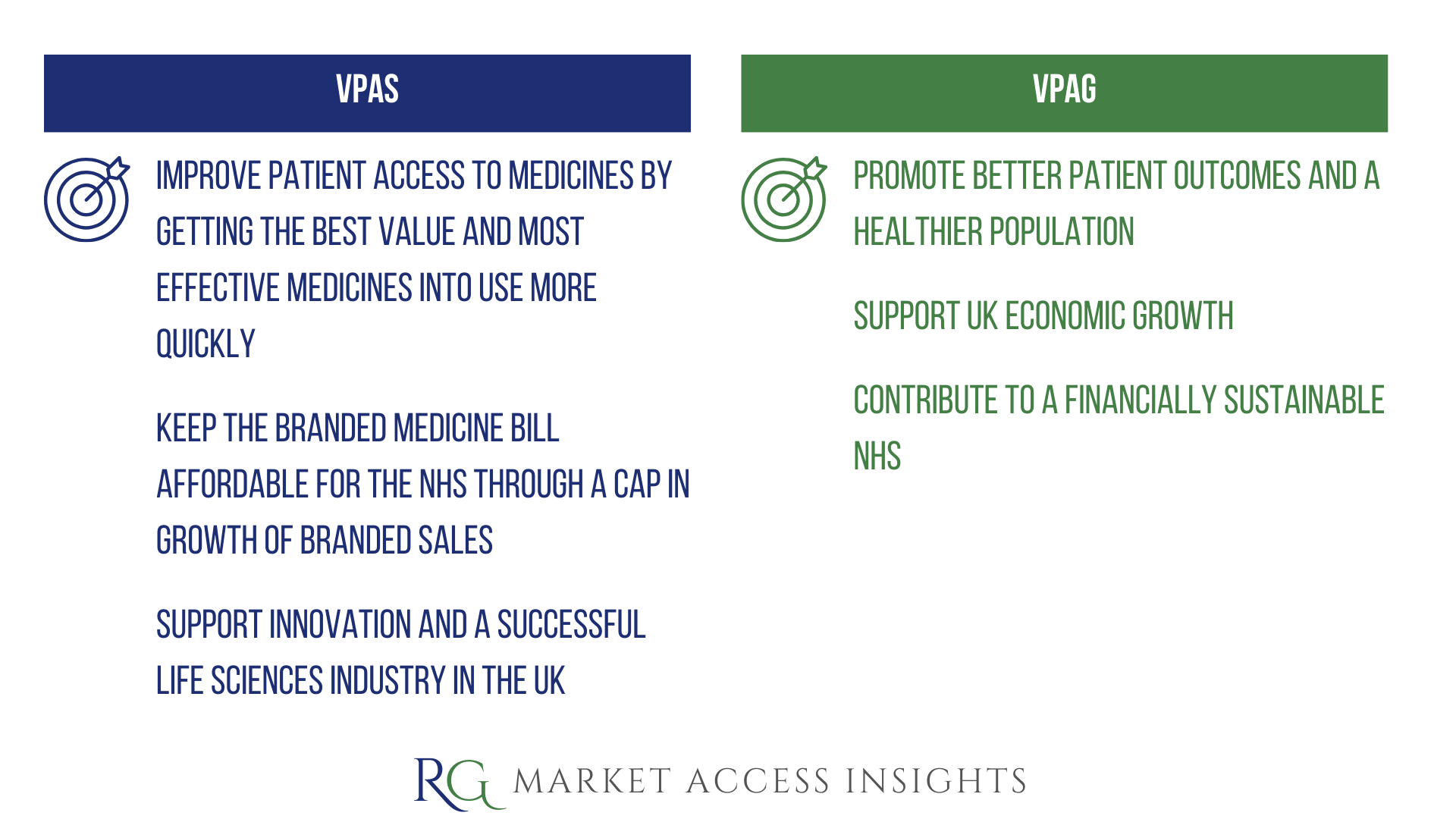

Objectives

Both schemes sought/will seek to improve patient access to innovative treatments, support the financial sustainability of the NHS, and advance the UK life sciences sector.

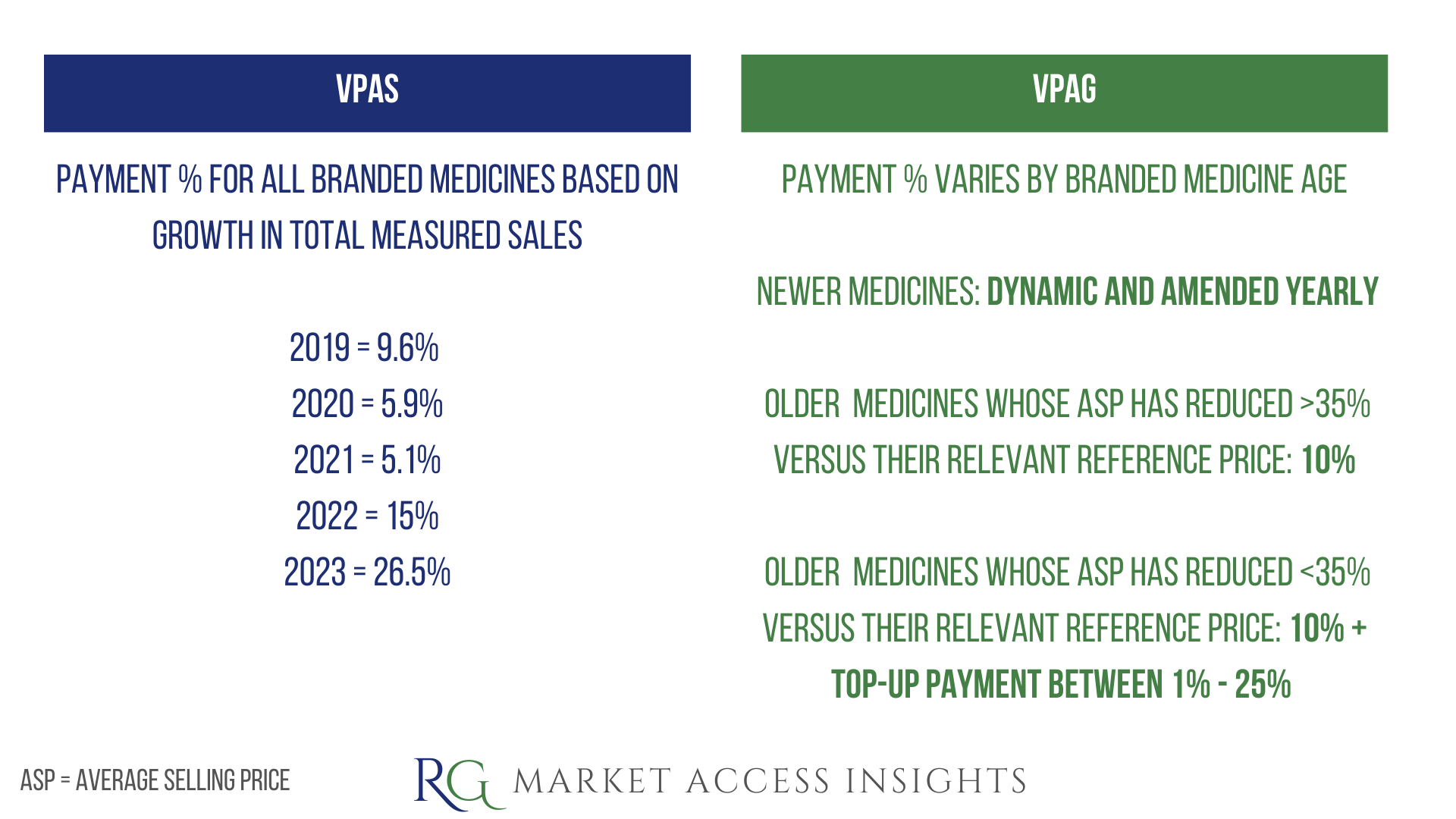

Payments and the Affordability Mechanism

Under both schemes, the pharmaceutical industry agrees to contribute to NHS financial sustainability through an allowed growth rate on the sales of branded health service medicines. Sales above the cap are paid back to the government by scheme members via a levy.

However, VPAG introduces differentiated payment mechanisms between newer and older medicines to both balance risk and account for the different lifecycle stages of a medicine.

Let’s not forget that a key objective of the Voluntary Scheme is for it to be financially more attractive than the Statutory Scheme for manufacturers with multiple innovative products in their portfolio. In 2023, the payment percentage difference between those two schemes was just 1% (26.5% and 27.5% for the Voluntary and Statutory Scheme respectively) leading to industry backlash. It’s hoped this new structure will resolve that issue and ensure that the Voluntary Scheme remains more financially attractive for manufacturers launching new active pharmaceutical ingredients (APIs) in the UK.

Note: neither scheme applies / will apply to sales of medicines for supply on private prescription or other use outside the NHS.

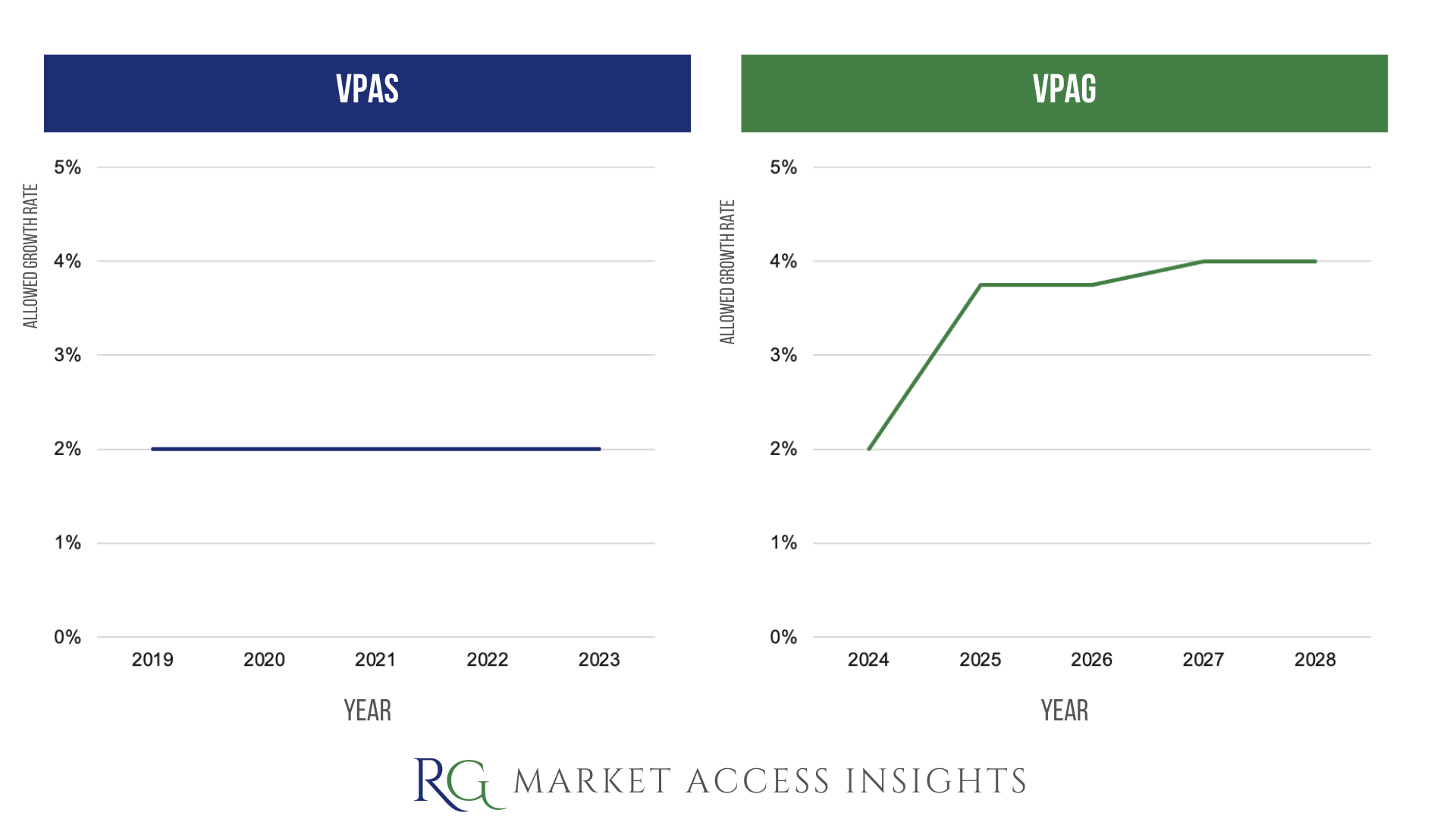

Allowed Growth Rate

VPAS capped branded medicines sales growth at a fixed rate of 2% over 5 years, whereasVPAG will allow the level of annual allowed growth in branded medicines sales to double from 2% in 2024 to 4% in 2027.

Savings Target

VPAS: no sum specified.

VPAG: the new landmark deal is anticipated to save the NHS £14 billion.

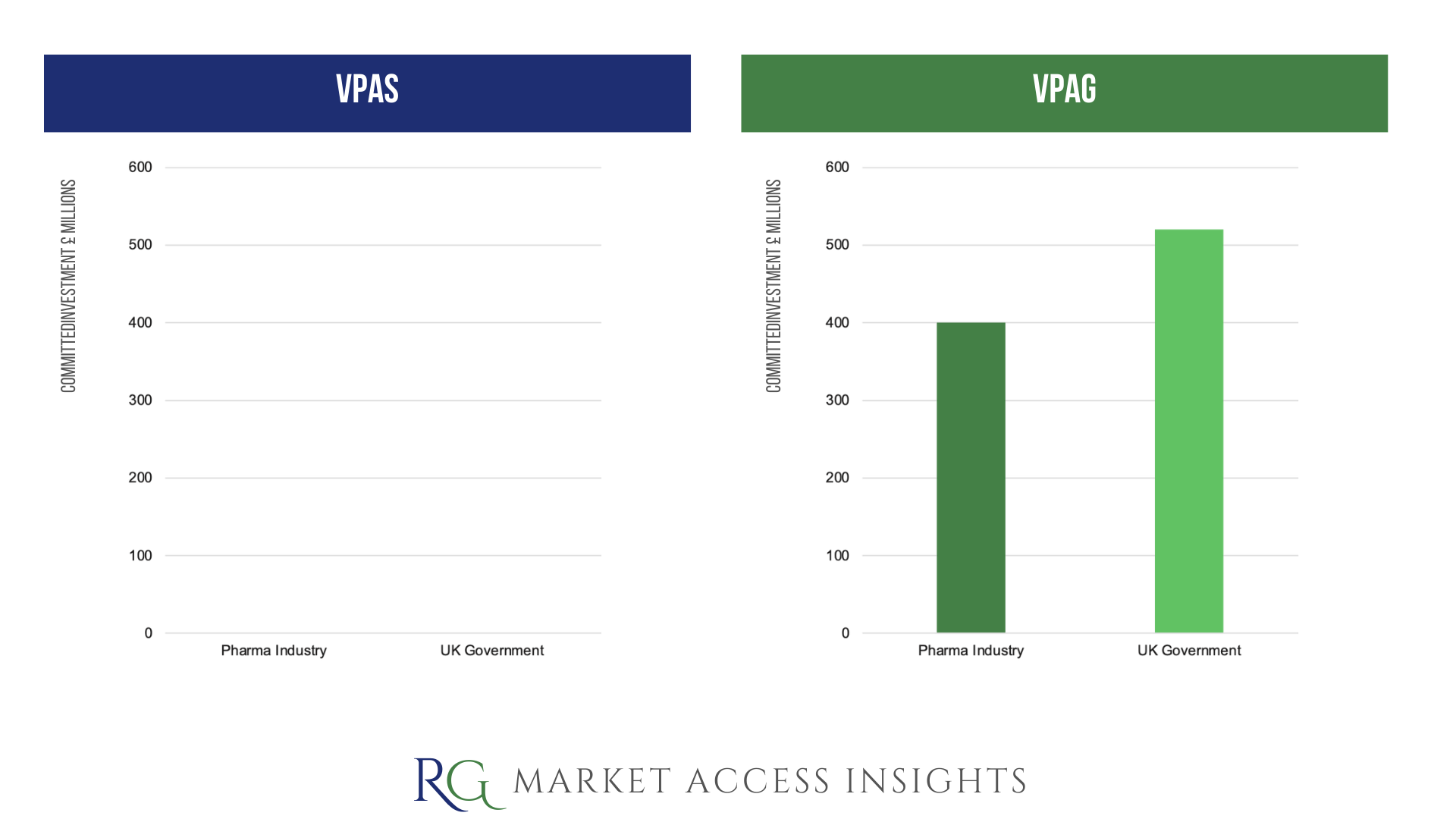

Investment

VPAS: no specific provisions or sums noted.

VPAG: there will be £400 million of investment by the pharmaceutical industry to support UK innovation, sustainability, and growth in:

Pioneering clinical trials (75%*)

Manufacturing (5%*)

Innovative health technology assessments (HTA) (20%*)

(*percentage of the funding allocation)

Additionally, £520 million of investment from the UK government will support Lifesciences manufacturing, and research and development.

Adoption of clinically and cost-effective medicines

VPAS: focuses on tracking adoption.

For example, it included a commitment to the continued development of measurement tools, such as the Innovation Scorecard, to track uptake and health outcomes.

VPAG: focuses on tracking equitable adoption.

NHS England will develop a local formulary national minimum dataset that seeks to improve equity in access to NICE recommendation treatments through increased visibility in local adoption variations.

Horizon scanning

Both schemes sought/will seek to enhance the NHS approach to horizon-scanning to improve planning and forecasting.

Under VPAG, the UK’s PharmaScan platform will be redeveloped, and scheme members will be committed to providing timely and accurate information on their pipeline.

NICE value assessments

Under both schemes, the standard cost-effectiveness threshold used by NICE is unchanged at £20,000 to £30,000 per Quality Adjusted Life Year (QALY).

Commercial arrangements

Here we see some differences, with VPAG showing a greater willingness from NHS England to engage with innovative payment models.

VPAS: commitment to increased commercial flexibility. For example, under VPAS NHS England developed innovative commercial incentives to tackle antimicrobial resistance.

VPAG: includes a commitment from NHS England to pilot 2 innovative payment models for advanced therapy medicinal products (ATMPs). Additionally, NHS England and NICE will review the threshold for the Budget Impact Test, and consult on whether it should be increased to £40 million.

Wrap Up

In summary, the key difference between the schemes is consistent with the new branding, a bigger focus on growth as seen by:

A willingness for the allowed growth rate to exceed 2% for the first time ever

A commitment to support UK economic growth through investment in Lifesciences manufacturing, research and development, clinical trials, and HTAs

A willingness to differentiate payments on new medicines to improve access and initiatives to track local uptake to ensure equitable adoption

“Millions of NHS patients will benefit from this momentous, UK-wide agreement. Not only will it save the health service billions of pounds every year, it will allow more patients to quickly access the latest life-saving medicines and treatments. This deal will also ensure the UK remains a world leader in driving forward innovative healthcare while boosting our economy, with hundreds of millions of pounds invested in vital research, clinical trials and manufacturing.”

Health and Social Care Secretary Victoria Atkins

If you found this blog post helpful, consider sharing it or subscribing :)

Cover photo credit: Photo by Michał Parzuchowski on Unsplash